Why Incentivize Private Lands Conservation?

United States

in private lands

Florida in

private lands

Georgia in

private lands

SAVING MONEY

It’s smart for the public to invest in private land conservation through tax incentives for conservation easements. While public lands are critically important, it is far more expensive to buy and manage land than protect land through conservation easement.

MAKING A DIFFERENCE

Thanks to incentives, almost 20 million acres of private land in the United States are permanently conserved with conservation easements. These protected private lands help ensure enough clean water, wildlife conservation, and open spaces.

Federal Tax incentives for Conservation Easements

FEDERAL INCOME TAX INCENTIVES

A conservation easement donation, whether partial or full, can qualify for a federal income tax deduction, similar to other charitable giving. Given the relatively high value of most conservation easement donations, a qualified conservation contribution can be used to:

- Deduct up to 50% of adjusted gross income (AGI) for the year of the donation.

- Qualified farmers and ranchers can deduct up to 100% of their AGI.

- Any unused deduction can be carried forward for an additional 15 years.

FEDERAL ESTATE BENEFITS

Land is often a significant asset within someone’s estate. Upon a person’s death, their land is valued for the estate at its current fair market value (not the original purchase price or basis). For 2018–2025, estates valued more than 11.2 million per individual or 22.4 million per couple will pay 40% estate tax, including land value.

A conservation easement can greatly reduce the value of the land for the estate. There are other potential federal estate tax incentives, such as IRC 2031(c), which can allow for an additional $500,000 in estate tax savings for conservation easement lands.

Estate planning is often complicated and best achieved with a qualified advisor. Consider talking with your advisor about conservation easements.

For more information and some great examples on the federal tax incentive for conservation easements, check out the Land Trust Alliance’s guide Using the Conservation Tax Incentive below.

This hay field is part of a

conservation easement in

Gadsden County, Florida. The

owner receives a 100%

exemption on his property taxes.

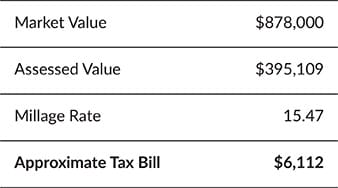

FLORIDA Tax Incentives for Conservation Easements

Scenario: 400-acre Property with agricultural fields, timber, and wetlands

This landowner maintains the property exclusively for its

conservation purposes with no commercial uses.

This conservation easement qualifies for a 100% exemption from

ad valorem taxes – the landowner’s tax bill is $0.

The Nunnallys donated a

conservation easement in Macon

County, Georgia. They received

the Georgia Conservation Tax

Credit for their donation.

Georgia Tax incentives for Conservation Easements

Conservation INCOME TAX Credit

Georgia offers a state income tax credit for up to 25% of the conservation easement value (based on an appraisal). The tax credit is capped at $250,000 for an individual and many types of pass-through corporations (LLCs, LLPs). For corporations (s-corp, c-corp) the tax credit cap is $500,000. The Georgia tax credit is transferrable (the credit can be sold).

To qualify for the tax credit, a conservation easement must meet at least 2 conservation purposes, protecting:

- Water quality

- Wildlife habitat

- Outdoor recreation

- Prime agricultural and forestry lands

- Cultural sites

The conservation easement appraisal must be reviewed and approved by the Georgia State Properties Commission. The conservation easement must held by an accredited land trust, such as Tall Timbers. There are other requirements that should be reviewed before considering the tax credit. Visit the Georgia Land Conservation Program website for more details.

Conservation Use Valuation Assessment (CUVA)

CUVA is designed to protect property owners from being pressured by the property tax burden to convert their land from agricultural use to residential or commercial use. Conservation easement lands can receive reduced ad valorem (county property) taxes through CUVA. Landowners must maintain their land in the designated use (conservation, agriculture, or forestry) for 10 years. CUVA is capped at 2,000 acres per landowner in a county. CUVA is administered by the tax assessor’s office in each county, and procedures differ by county. Contact your county office or the Georgia Department of Revenue for details.

Forest Land Protection Act (FLPA)

FLPA is similar to CUVA, but it is designed for larger forest landowners. Conservation easement lands with a prevalence of forests can receive reduced county property (ad valorem) taxes. A property must be at least 200 acres to qualify for FLPA, but there is no cap on maximum acres. Landowners must maintain their land in forestry use for 15 years. FLPA is administered by the tax assessor’s office in each county. Contact your county office for details.

For more information on Georgia conservation incentives,

visit the Georgia Department of Natural Resources